DEAL THESIS CANNOT RELY ON RATES DROPPING…OR RENTS MAGICALLY INCREASING.

A word on rates.

Many still anticipate the elusive Federal Reserve rate cuts later this year. And although the Fed may still cut rates, generally rates are cut when an economy is weak or feared to weaken. By most accounts, we’re not there yet.

According to the Federal Bureau of Labor Statistics, employment growth was surprisingly strong in May, as employers added 272,000 jobs. This was far above consensus expectations of 180,000 in a market that had shown signs of cooling.

The rebalancing of the labor market, in combination with a cooling but stable economy, gives the Federal Reserve reason to be patient before cutting the federal funds rate. This is likely to disappoint (…) investors and lenders in the commercial real estate market. (Source: Costar 6/12/24)

That, taken with the understanding that current interest rates aren’t high by historic standards, means that deal thesis cannot rely on rates decreasing substantially. That’s not to say the Fed will not cut rates, but what seemed a foregone conclusion twelve months ago is not so much now.

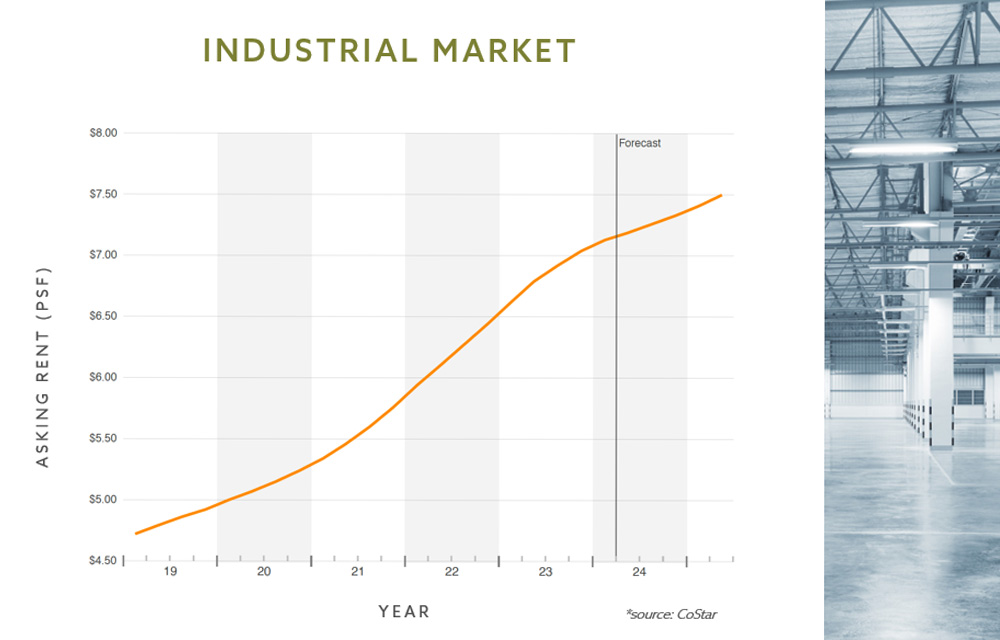

Now rents.

Over the past several years the ‘mark to market’ concept or ‘forced appreciation’ has been core to many real estate investment strategies. Rents have indeed increased, perhaps nearly two-fold since pre-Covid, for certain asset classes in certain markets. Generally, rent growth is now at the top of the “S” curve. Tenants are not able to, and will not, absorb unlimited rent increases. They will do more with less or their business models will evolve to require less space—or no space.

Increases in pass-through expenses or TICAM are also stressing occupancy costs. We’re working on several assignments where TICAM is over $10/SF and shocking to some users, who expect perhaps half that. Increases in taxes, notably in insurance and other costs, are increasing tenants’ gross occupancy costs, and eroding net operating income for landlords and investors.

The takeaway: investors can’t count on decreasing interest rates or drastically increasing rents to underwrite deals—or bail them out of struggling projects.

{kind=link}